Steel Pricing in Transition: What Industrial Construction Should Expect in 2026

Executive Summary

Steel pricing has moved out of the crisis phase, but it has not returned to “normal.”

After the extreme volatility of 2021–2022, Producer Price Index (PPI) data shows moderation across key steel products — iron and steel mills, pipe and tube, and rolled steel shapes — yet prices remain structurally elevated compared to pre-2020 levels.

For industrial construction teams, this shift matters. The challenge is no longer reacting to sudden price spikes, but managing ongoing uncertainty across budgeting, procurement timing, and schedule risk. In this environment, steel pricing has become a strategic input rather than a background assumption.

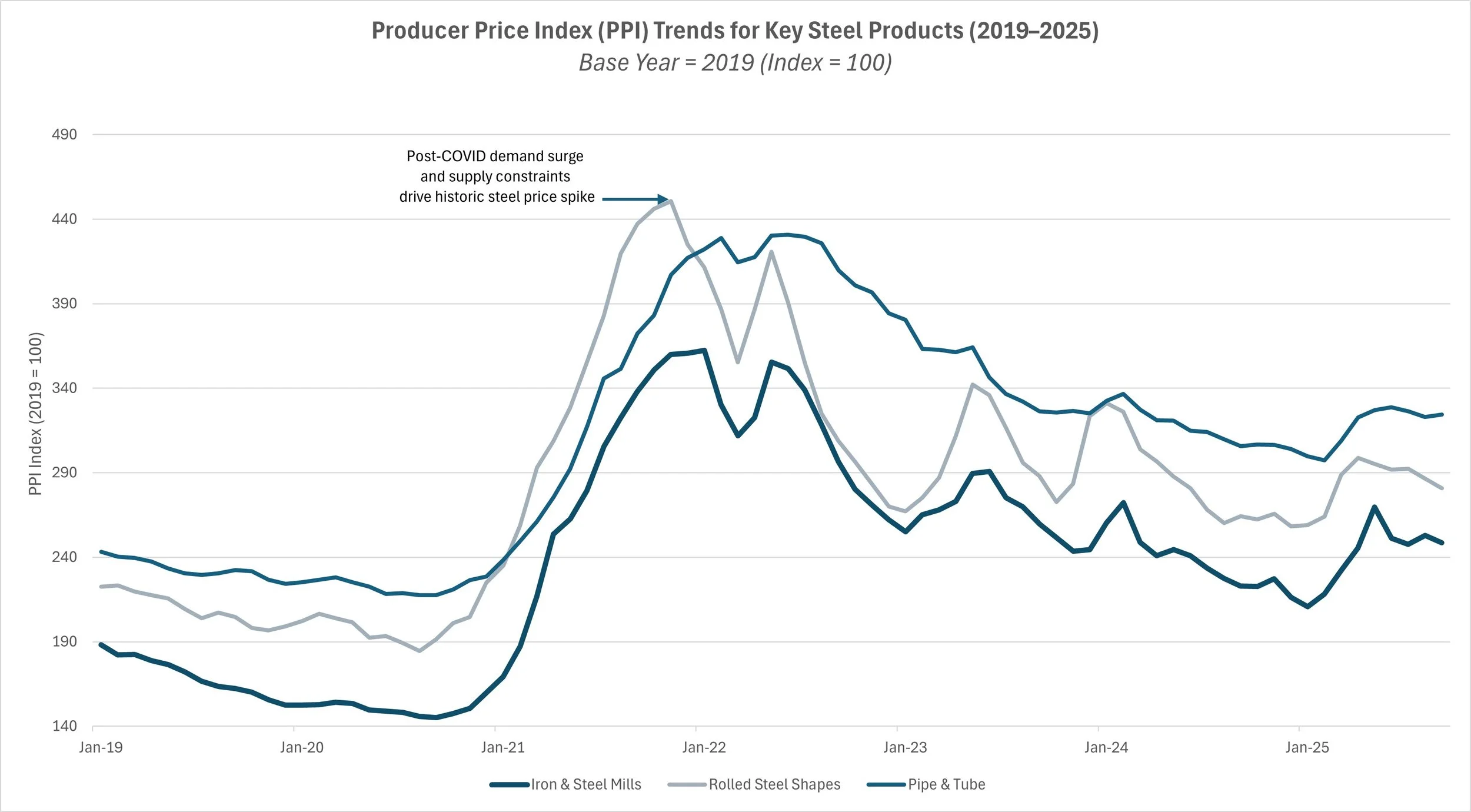

Figure 1: Producer Price Index (PPI) trends for key steel products show a historic post-COVID price surge in 2021–2022 followed by partial normalization and continued volatility

Where Steel Prices Stand Today

Recent BLS Producer Price Index trends illustrate a clear pattern:

A historic spike in steel prices during the post-COVID recovery, driven by demand surges and supply constraints

A steady pullback through 2023–2024 as capacity improved and demand normalized

Continued price levels in 2025 that remain meaningfully above 2019 baselines

While month-to-month volatility has eased, indexed steel prices have not reverted to pre-pandemic norms. ENR construction cost indicators reinforce this reality: materials pricing has stabilized, but at a higher cost floor that project teams must now plan around.

Key takeaway: moderation does not equal predictability.

Figure 1: Producer Price Index (PPI) trends for key steel products show a historic post-COVID price surge in 2021–2022 followed by partial normalization and continued volatility.

What’s Driving Ongoing Volatility

Several structural factors continue to influence steel pricing:

Energy and production costs

Steel remains energy-intensive. Fluctuations in electricity, natural gas, and fuel costs directly affect mill pricing and fabrication costs.

Global supply dynamics

Imports, tariffs, and international production shifts continue to influence domestic availability and pricing leverage.

Domestic capacity and lead times

Even with improved supply, mill utilization rates and fabrication backlogs can quickly translate into schedule risk for large industrial projects.

Policy and sustainability pressures

Programs like California’s Buy Clean Act and broader EPD requirements are reshaping procurement decisions. Low-carbon steel options may carry cost premiums or limited availability, adding another layer of complexity to pricing assumptions.

This is why headline narratives about “stable steel prices” often fail to reflect real-world delivery risk.

Implications for Industrial & Warehouse Projects (Southern California)

For industrial and logistics projects, steel pricing uncertainty shows up early and often:

Feasibility & early budgeting: indexed assumptions matter more than spot pricing

Schedule risk: long-lead steel items remain a critical path driver

Contract strategy: escalation clauses and procurement timing are under closer scrutiny

Southern California adds additional pressures:

Heavy port activity and logistics demand

Persistent labor constraints

Continued demand for warehouse and industrial space

In this market, small misalignments in steel procurement strategy can create outsized cost and schedule impacts.

What Project Teams Can Do Now

Leading teams are shifting from reactive adjustments to proactive planning:

Making steel procurement decisions earlier in the design phase

Evaluating alternative detailing or material strategies where feasible

Improving coordination between design, estimating, and procurement teams

Treating steel pricing as a managed risk, not a fixed input

The goal is not to predict prices perfectly, but to reduce exposure through better timing and alignment.

Looking Ahead to 2026

Steel pricing will remain a strategic variable heading into 2026. While the extreme volatility of recent years has passed, structural pressures — from energy costs to sustainability requirements — are unlikely to disappear.

Owners and developers should watch:

PPI trend movements across steel subcategories

Capacity utilization and fabrication lead times

Policy developments affecting low-carbon materials

Understanding these signals early will be essential to maintaining schedule certainty and cost control.

Next up: a deeper look at construction confidence indicators and what they signal for 2026 project pipelines.