Bridging the Gap Between Embodied Carbon Policy and On-Site Practice

The built environment sits at the heart of the world’s decarbonization challenge. Globally, buildings account for roughly 37% of all CO₂ emissions — about a tenth of that tied not to operations, but to the materials and processes used to build them. This “embodied carbon” has become construction’s quiet frontier. Over the past few years, we’ve seen an undeniable shift from discussion to action. Governments are passing Buy Clean laws, investors are embedding ESG expectations, and major contractors are setting carbon reporting requirements. Yet on the jobsite, many teams are still asking the same question: How do we actually make this work?

1. Policy Momentum Is Real — and Accelerating

The policy side of embodied carbon has never moved faster. California’s Buy Clean Act set the standard, requiring Environmental Product Declarations (EPDs) and carbon limits for materials like steel and glass. At least 14 states are now following suit with low-carbon procurement laws, while the Environmental Protection Agency has launched a $350 million initiative to expand EPD data for U.S. manufacturers.

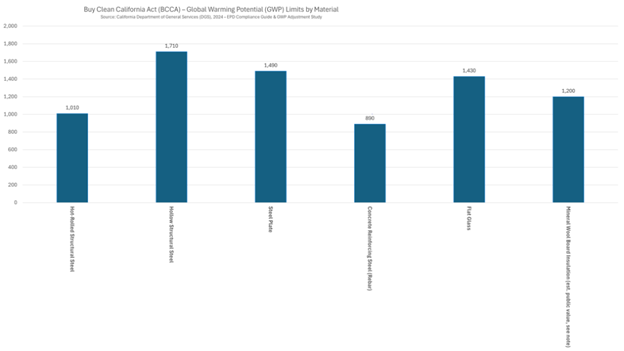

California continues to lead in embodied-carbon policy through the Buy Clean California Act, which sets material-specific Global Warming Potential (GWP) limits for state-funded projects.

These limits, developed by the Department of General Services (DGS), establish baseline emissions targets for structural steel, glass, and insulation—effectively linking procurement with lifecycle carbon accountability.

Figure 1 shows the most recent published GWP thresholds by material under the 2024–2025 adjustment study.

Figure 1: California’s Buy Clean Act establishes Global Warming Potential (GWP) limits for key construction materials, source: California Department of General Services (DGS), 2024 EPD Compliance Guide & 2025 GWP Adjustment Study.

Industry organizations are reinforcing the push. The Associated General Contractors of America released its 2024 Decarbonization Playbook, aligning project reporting with the Greenhouse Gas Protocol and introducing clear steps for contractors to define accountability across Scopes 1–3. The International Code Council and McKinsey’s joint work has also shown that buildings could cut emissions by up to 75% by 2050 with existing technologies if codes, policies, and enforcement align.

On the private side, ESG expectations have become a market force. Construction Dive recently reported that investors and lenders are using sustainability performance as a key risk metric for multifamily development. And in the residential sector, NAHB’s 2024 survey found that more than 60% of homebuilders expect the majority of their projects to include sustainable features by 2026.

It’s clear: regulation, investment, and consumer demand are finally pulling in the same direction. The challenge now is making these ambitions practical on-site.

2. The Jobsite Reality Check

For many contractors, sustainability feels both essential and elusive. ENR’s 2025 Cost Report placed the Construction Confidence Index at 48 — a sign of cautious optimism amid tight margins, rising materials prices, and persistent labor shortages. BLS and Federal Reserve data show that while construction employment is growing, workforce capacity for specialized sustainability roles remains limited.

That’s why education and training have become a central piece of the puzzle. Early this year, Skanska and Fluor launched a digital “sustainability school” to teach project teams how to integrate carbon accounting, ESG documentation, and low-carbon procurement into daily workflows. It’s a practical move that begins to close the gap between policy goals and field execution.

At the same time, the AGC Playbook reminds us that progress starts with data. The guide urges contractors to track emissions across all project phases — from material extraction (A1) to onsite energy and waste (A5) — and to request verified EPDs from suppliers. These practices aren’t just paperwork; they’re the foundation of measurable decarbonization.

In short, the construction workforce is ready and willing — it just needs the right mix of knowledge, tools, and consistent client expectations.

3. Innovation and Opportunity on the Ground

Across the industry, the technology to bridge policy and practice already exists — it’s just not evenly adopted yet.

Skanska’s 2019 development of the EC3 carbon calculator, and Procore’s 2022 integration of it into everyday project management software, made embodied-carbon tracking accessible to contractors. McKinsey’s work on materials shows why that matters: with today’s technologies, the industry could halve embodied emissions by 2030, and innovations like low-carbon steel have the potential to cut up to 90% of material emissions without sacrificing performance.

Corporations are stepping up too. Amazon’s new mass-timber delivery facility is being built as a “sustainability lab,” testing how renewable materials perform at industrial scale. Michigan’s newly announced mass-timber incentive program shows state governments can encourage the same shift. And manufacturers are proving what’s possible: DuPont’s 2025 sustainability report revealed up to 93% greenhouse-gas reductions across select Corian® product lines through improved manufacturing and sourcing.

Even early innovators like Kraft Heinz — which in 2021 began turning recycled plastic packaging into roofing panels — remind us that every small experiment contributes to the larger movement.

Collectively, these examples point toward a future where sustainability isn’t an add-on — it’s simply how construction is done.

4. Closing the Gap

When we zoom out, it’s clear that embodied-carbon policy and on-site practice are finally starting to converge. Policies like Buy Clean are creating the demand signals, while digital tools, better data, and cross-sector collaboration are making it possible to respond.

The next step is consistency — in measurement, education, and procurement. Building codes, contracts, and specifications must begin to speak the same carbon language. As the AGC and ICC have both emphasized, success depends on integrating carbon accountability into the same systems we already use for safety, quality, and cost.

This is a moment of genuine opportunity. The construction industry has the technology, the data, and now the mandate. Bridging the gap between policy and practice isn’t about adding new burdens; it’s about building smarter, cleaner, and more transparently than ever before.

Let’s keep the momentum moving from policy to project, from commitment to construction.

What’s one practical step your team has taken to measure or reduce embodied carbon?